Who are these accounts for?

Our School Cash Deposit Manager Accounts are suitable for any school in the United Kingdom.

We support schools in achieving the best returns for any cash balances they are holding, whether Fees in Advance or simply high cash balances at the beginning of term.

In particular, our accounts avoid the risks posed by the FSCS limit because all of the funds are simply deposited liquid and unencumbered at the Bank of England, where they are held in cash and never loaned or used by any institution to make money. This means that charities with significant cash holdings can enjoy a great return on those funds but without any additional risk.

Our Private Bank-Beating Interest Rates

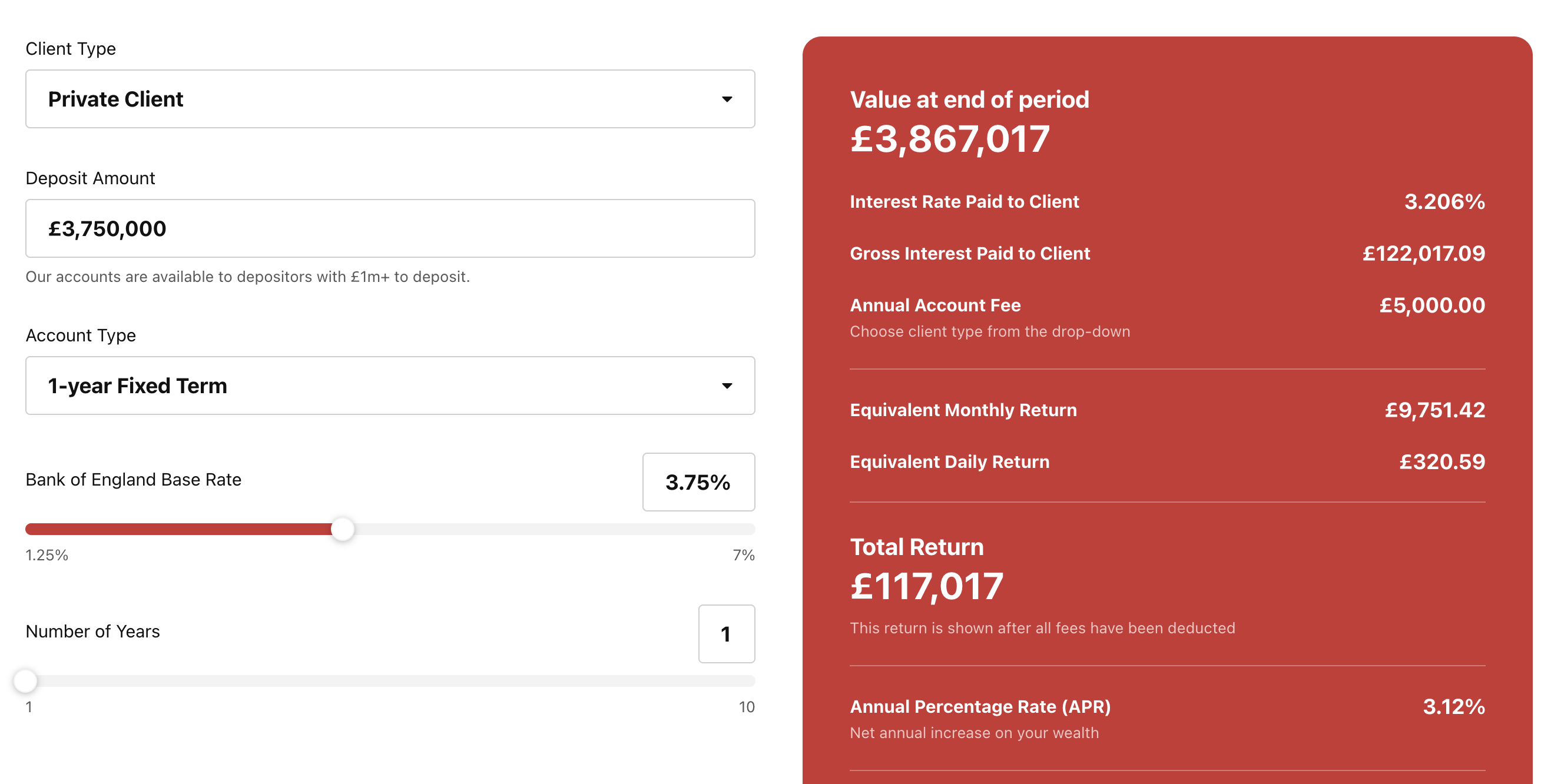

Notice Account

1

-month

2.87%

gross

2.91%

AER

Notice Account

3

-month

3.04%

gross

3.07%

AER

Fixed-Term Deposit

12

-month

3.21%

gross

3.21%

AER

Independent Schools

.jpeg)